The Real Bottleneck in the Humanoid Race

Matthieu Benat

•

The Real Bottleneck in the Humanoid Race

Matthieu Benat

•

The Real Bottleneck in the Humanoid Race

Matthieu Benat

•

Introduction

The technology case for humanoid robots is getting harder to argue against. AI models are improving faster than most roadmaps anticipated, and capital continues to flow into the sector at scale. On the engineering side, the question is no longer whether humanoids will work, it's whether they can be manufactured and deployed economically at scale.

A landmark McKinsey analysis on humanoid supply chain economics puts the challenge in sharp relief. The cost and sourcing constraints behind humanoid hardware are, in many ways, more daunting than the technical ones. And at the center of it all sits a component most engineers rarely think about: the actuator.

The Actuator Problem

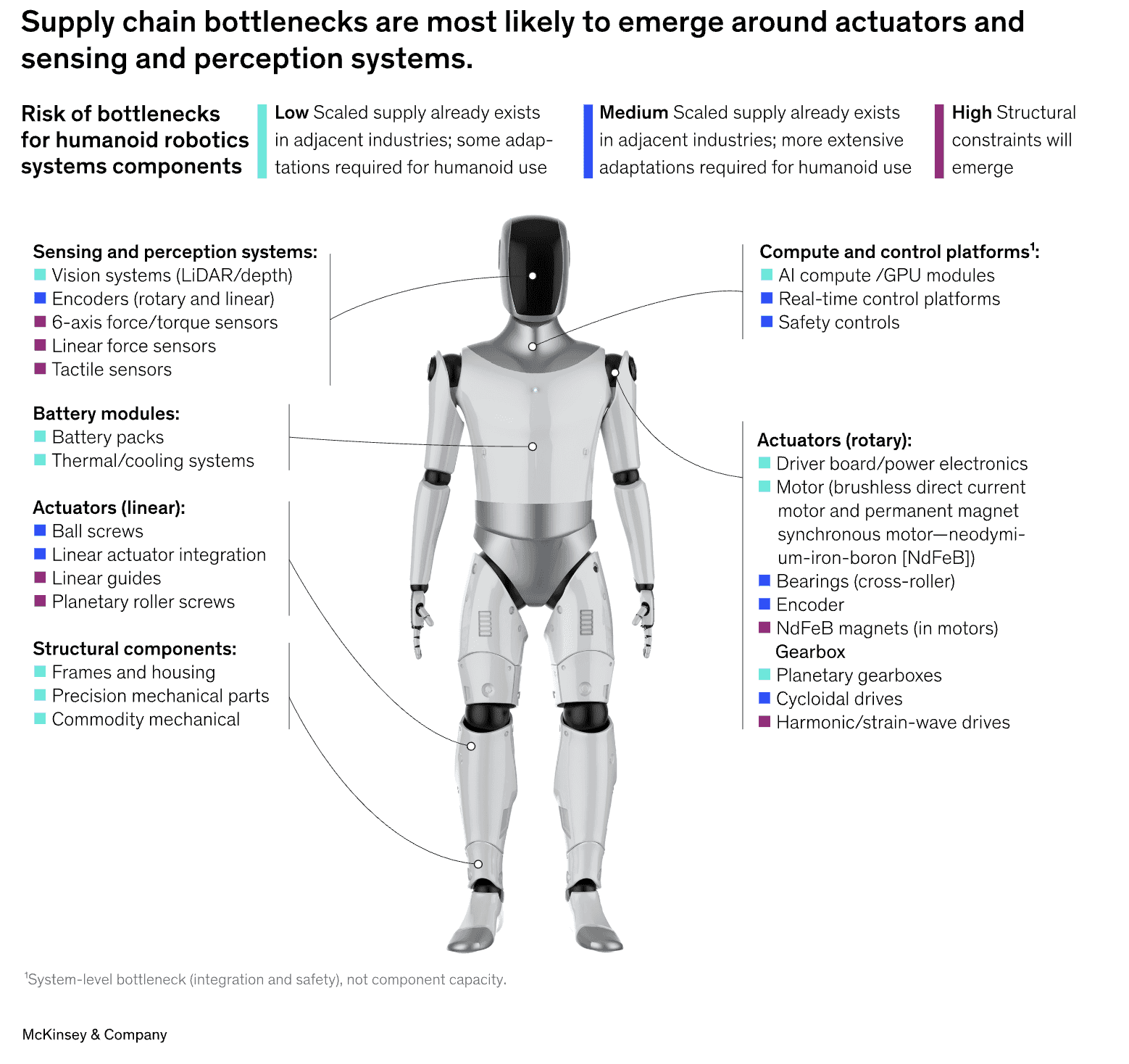

Actuators (the electromechanical systems that drive a robot's joints and limbs) represent the single largest cost slice in a humanoid robot's BOM. They are also, by a significant margin, the component category with the least mature supplier ecosystem in the entire hardware stack.

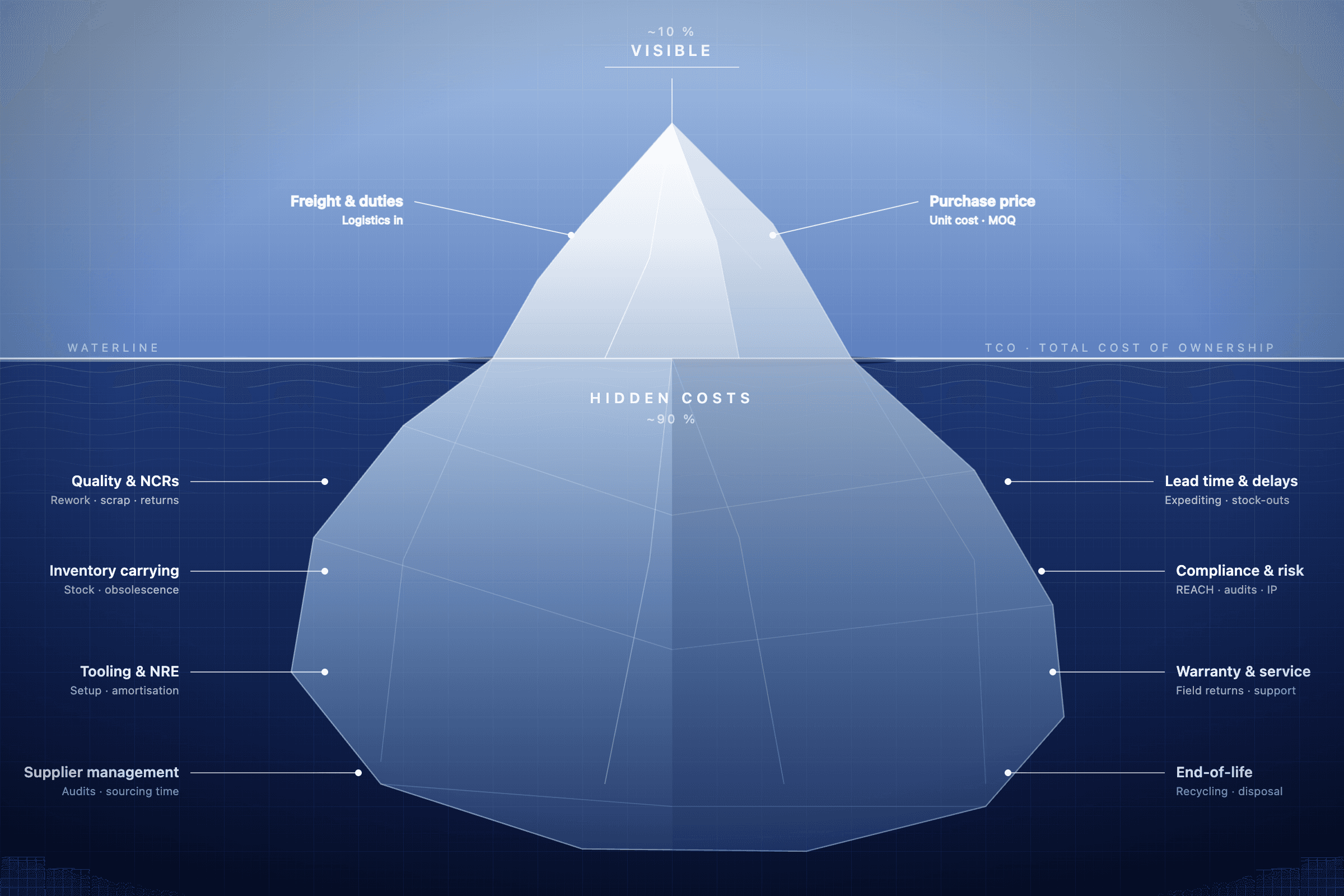

This matters for two reasons. First, BOM cost needs to fall from a current range of $30,000–$150,000 to under $20,000 for humanoids to reach mass deployment viability. Second, achieving that cost reduction requires suppliers who can deliver precision components at volume and those suppliers, for the most critical parts, are overwhelmingly concentrated in a single geography.

The Geography of Dependence

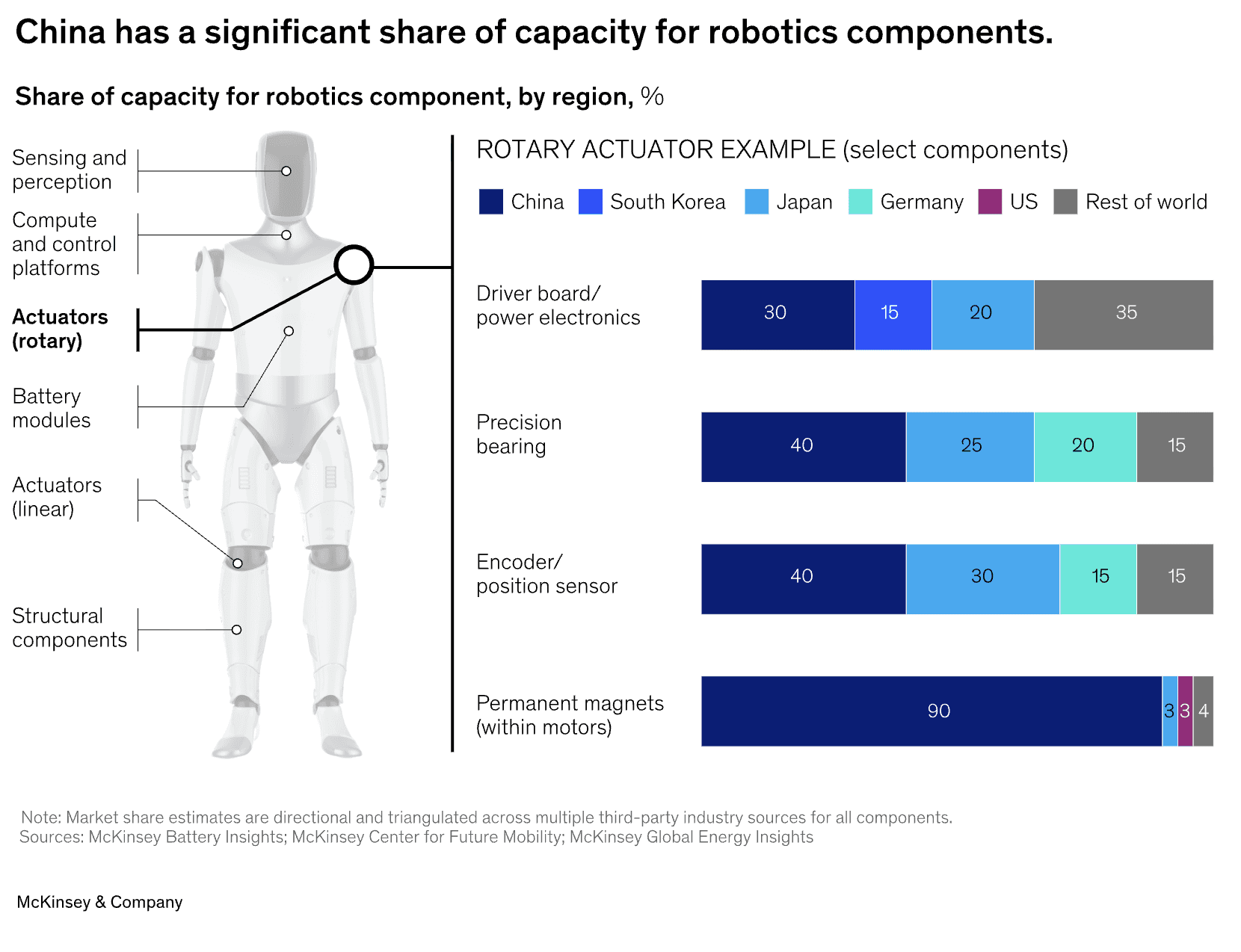

China produces approximately 90% of the permanent magnets that humanoid actuators depend on. 40% of precision bearings also come from Chinese suppliers. These are not peripheral components they are structural inputs without which the hardware stack cannot function.

For robotics companies headquartered in the EU or the US, this creates a sourcing posture that is difficult to describe as anything other than fragile. A single geopolitical disruption, export restriction, or supply shock in the magnet or bearing supply chain ripples immediately into production schedules, unit economics, and time-to-market.

A Sourcing Problem Dressed as a Tech Problem

The framing that dominates robotics investment and media coverage treats hardware cost reduction as primarily an engineering challenge better designs, tighter tolerances, smarter integration. That framing is incomplete.

The deeper constraint is supplier development. Building a resilient, multi-tier supplier network for components that do not yet have a mature market is a procurement challenge. It requires early supplier qualification, dual-source strategies from the outset, and the ability to assess supplier capability against specifications that themselves are still evolving.

This is what NPI sourcing looks like at its hardest: qualifying suppliers for components where no established vendor ecosystem exists, under cost and time-to-market pressure, with geopolitical risk baked into the baseline.

What Would It Take for the EU and the US to Stand a Chance?

Answering that question seriously means moving beyond industrial policy declarations and into the operational specifics of supplier development. It means identifying where alternative magnet and bearing supply chains could realistically be built and at what cost premium relative to Chinese sources. It means investing in supplier qualification infrastructure, not just R&D subsidies.

It also means treating procurement as a strategic function rather than a cost center. The companies that will lead in humanoid robotics will not simply be those with the most capable AI or the most elegant mechanical design. They will be the ones who built the supplier relationships, qualification processes, and sourcing intelligence needed to manufacture at scale before their competitors did.

Platforms like Siembra are being built precisely for this context: helping industrial procurement teams manage the complexity of NPI sourcing, from supplier qualification through BOM cost tracking, in environments where the supplier ecosystem is still taking shape.

Source

Introduction

The technology case for humanoid robots is getting harder to argue against. AI models are improving faster than most roadmaps anticipated, and capital continues to flow into the sector at scale. On the engineering side, the question is no longer whether humanoids will work, it's whether they can be manufactured and deployed economically at scale.

A landmark McKinsey analysis on humanoid supply chain economics puts the challenge in sharp relief. The cost and sourcing constraints behind humanoid hardware are, in many ways, more daunting than the technical ones. And at the center of it all sits a component most engineers rarely think about: the actuator.

The Actuator Problem

Actuators (the electromechanical systems that drive a robot's joints and limbs) represent the single largest cost slice in a humanoid robot's BOM. They are also, by a significant margin, the component category with the least mature supplier ecosystem in the entire hardware stack.

This matters for two reasons. First, BOM cost needs to fall from a current range of $30,000–$150,000 to under $20,000 for humanoids to reach mass deployment viability. Second, achieving that cost reduction requires suppliers who can deliver precision components at volume and those suppliers, for the most critical parts, are overwhelmingly concentrated in a single geography.

The Geography of Dependence

China produces approximately 90% of the permanent magnets that humanoid actuators depend on. 40% of precision bearings also come from Chinese suppliers. These are not peripheral components they are structural inputs without which the hardware stack cannot function.

For robotics companies headquartered in the EU or the US, this creates a sourcing posture that is difficult to describe as anything other than fragile. A single geopolitical disruption, export restriction, or supply shock in the magnet or bearing supply chain ripples immediately into production schedules, unit economics, and time-to-market.

A Sourcing Problem Dressed as a Tech Problem

The framing that dominates robotics investment and media coverage treats hardware cost reduction as primarily an engineering challenge better designs, tighter tolerances, smarter integration. That framing is incomplete.

The deeper constraint is supplier development. Building a resilient, multi-tier supplier network for components that do not yet have a mature market is a procurement challenge. It requires early supplier qualification, dual-source strategies from the outset, and the ability to assess supplier capability against specifications that themselves are still evolving.

This is what NPI sourcing looks like at its hardest: qualifying suppliers for components where no established vendor ecosystem exists, under cost and time-to-market pressure, with geopolitical risk baked into the baseline.

What Would It Take for the EU and the US to Stand a Chance?

Answering that question seriously means moving beyond industrial policy declarations and into the operational specifics of supplier development. It means identifying where alternative magnet and bearing supply chains could realistically be built and at what cost premium relative to Chinese sources. It means investing in supplier qualification infrastructure, not just R&D subsidies.

It also means treating procurement as a strategic function rather than a cost center. The companies that will lead in humanoid robotics will not simply be those with the most capable AI or the most elegant mechanical design. They will be the ones who built the supplier relationships, qualification processes, and sourcing intelligence needed to manufacture at scale before their competitors did.

Platforms like Siembra are being built precisely for this context: helping industrial procurement teams manage the complexity of NPI sourcing, from supplier qualification through BOM cost tracking, in environments where the supplier ecosystem is still taking shape.

Source

Introduction

The technology case for humanoid robots is getting harder to argue against. AI models are improving faster than most roadmaps anticipated, and capital continues to flow into the sector at scale. On the engineering side, the question is no longer whether humanoids will work, it's whether they can be manufactured and deployed economically at scale.

A landmark McKinsey analysis on humanoid supply chain economics puts the challenge in sharp relief. The cost and sourcing constraints behind humanoid hardware are, in many ways, more daunting than the technical ones. And at the center of it all sits a component most engineers rarely think about: the actuator.

The Actuator Problem

Actuators (the electromechanical systems that drive a robot's joints and limbs) represent the single largest cost slice in a humanoid robot's BOM. They are also, by a significant margin, the component category with the least mature supplier ecosystem in the entire hardware stack.

This matters for two reasons. First, BOM cost needs to fall from a current range of $30,000–$150,000 to under $20,000 for humanoids to reach mass deployment viability. Second, achieving that cost reduction requires suppliers who can deliver precision components at volume and those suppliers, for the most critical parts, are overwhelmingly concentrated in a single geography.

The Geography of Dependence

China produces approximately 90% of the permanent magnets that humanoid actuators depend on. 40% of precision bearings also come from Chinese suppliers. These are not peripheral components they are structural inputs without which the hardware stack cannot function.

For robotics companies headquartered in the EU or the US, this creates a sourcing posture that is difficult to describe as anything other than fragile. A single geopolitical disruption, export restriction, or supply shock in the magnet or bearing supply chain ripples immediately into production schedules, unit economics, and time-to-market.

A Sourcing Problem Dressed as a Tech Problem

The framing that dominates robotics investment and media coverage treats hardware cost reduction as primarily an engineering challenge better designs, tighter tolerances, smarter integration. That framing is incomplete.

The deeper constraint is supplier development. Building a resilient, multi-tier supplier network for components that do not yet have a mature market is a procurement challenge. It requires early supplier qualification, dual-source strategies from the outset, and the ability to assess supplier capability against specifications that themselves are still evolving.

This is what NPI sourcing looks like at its hardest: qualifying suppliers for components where no established vendor ecosystem exists, under cost and time-to-market pressure, with geopolitical risk baked into the baseline.

What Would It Take for the EU and the US to Stand a Chance?

Answering that question seriously means moving beyond industrial policy declarations and into the operational specifics of supplier development. It means identifying where alternative magnet and bearing supply chains could realistically be built and at what cost premium relative to Chinese sources. It means investing in supplier qualification infrastructure, not just R&D subsidies.

It also means treating procurement as a strategic function rather than a cost center. The companies that will lead in humanoid robotics will not simply be those with the most capable AI or the most elegant mechanical design. They will be the ones who built the supplier relationships, qualification processes, and sourcing intelligence needed to manufacture at scale before their competitors did.

Platforms like Siembra are being built precisely for this context: helping industrial procurement teams manage the complexity of NPI sourcing, from supplier qualification through BOM cost tracking, in environments where the supplier ecosystem is still taking shape.